|

| ||||||

|

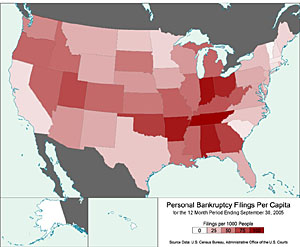

In this early version of "buy now pay later," "There was a rapid increase in reliance on personal finance companies for just arranging small loans for consumption and that growth was very importantly connected to a relaxing of usury laws in a great many states," says Edward Balleisen of Duke University. The next surge in filings, this time a six-fold gain, came during America's economic Golden Age, the '50s and '60s. "In this case," says Balleisen, "the growth in consumer credit is powerfully tied to the emergence of the change card and then the credit card." After 1985 came an era of rapid technological change, relatively low unemployment, and the further democratization of credit. And personal bankruptcies rose five-fold. The new law doesn't squelch the availability of credit. Far from it. It could even encourage credit card companies and other lenders to loosen their standards more. Instead, the idea was to cut down on Chapter 7 liquidations. But some economists are skeptical about whether it will. "If you think the of problem as being that certain people would look very creditworthy-and by being very creditworthy I mean having high income-get a huge amount of credit, and then file for bankruptcy and not pay their bills, then, well, the new law did a good job for those people," says UC San Diego economist Michelle White. "It made it a lot harder to file for bankruptcy." Yes, debtors with high earnings will find the stringent Chapter 13 repayment requirements unappealing. It won't be as easy for multimillionaires to shelter assets in mansions bought in states with high homestead exemptions, such as Florida and Texas. But the majority of filers live below their state's median income. Nationally, that figure is under $45,000. "If you think of the problem as being people who are lower down on the income scale, then I think most people will still file under Chapter 7 and things won't be very different than they were before," says White. "So it doesn't look like this is really going to increase credit card lenders' profits." So the law may not turn out to be a profit boon to the credit card companies that pushed for it. And it may not cut down on filers, says Elizabeth Warren of Harvard University. "Congress can pass all the laws it wants, but it won't change the underlying economic realty."

Continue to part 2 |

||||||